Wells Fargo’s new CEO: ‘We will get it done’

CEO Charlie Scharf has instilled the company with a sense of urgency in addressing its priorities.

CEO Charlie Scharf has instilled the company with a sense of urgency in addressing its priorities.

The Board of Directors of Wells Fargo has named Charles W. Scharf as the company’s CEO and president, effective October 21.

Bill Daley, who starts Nov. 13, will serve on the Operating Committee and will report directly to CEO Charlie Scharf.

CEO Charlie Scharf has instilled the company with a sense of urgency in addressing its priorities.

The Board of Directors of Wells Fargo has named Charles W. Scharf as the company’s CEO and president, effective October 21.

Bill Daley, who starts Nov. 13, will serve on the Operating Committee and will report directly to CEO Charlie Scharf.

In his first few months on the job, CEO Charlie Scharf has instilled the company with a sense of urgency in addressing its priorities. Changes have included bringing on new leaders from outside the company, reorganizing the company’s structure to ensure clear responsibility and accountability at every level, committing to additional investments in employees, and strengthening the company’s ability to manage risk.

On Feb. 21, we announced that we have entered into agreements with the United States Department of Justice and the United States Securities and Exchange Commission to resolve these agencies’ investigations into the company’s historical Community Bank sales practices and related disclosures. As part of this resolution, Wells Fargo has agreed to make payments totaling $3 billion.

On Feb. 11, we announced the appointment of several new business leaders and changes designed to create a flatter line of business organizational structure and provide leaders with clear authority, accountability, and responsibility.

“The Wells Fargo franchise has extraordinary opportunity and power, and these organizational changes enable us to more effectively pursue our goals and take advantage of the opportunities in front of us,” CEO Charlie Scharf said. “These changes create the right structure to build our businesses over the long term and increase our ability to successfully execute on our top priority, which is the risk, regulatory, and control work. I am confident that this organizational model and our strengthened risk and control foundation will bring greater focus and accountability to the company.”

Additionally, we are making fundamental changes to the way we manage operations, which will enable us to strengthen how we serve clients and customers, drive operational excellence, and execute on regulatory priorities. We are also creating a new Strategy, Digital Platform & Innovation group to enhance our focus on planning for the digital future and investing in the customer experience.

On Feb. 11, we announced that Mike Weinbach will join the company as CEO of Consumer Lending in early May, reporting to CEO Charlie Scharf. Weinbach spent 16 years at JPMorgan Chase where he was most recently CEO of Chase Home Lending. Previously at Chase he held leadership roles across Consumer Banking, Business Banking, Home Lending and Auto Finance in sales, finance, branch management and operations.

On Feb. 4, we announced Michael Cleary as head of Sales Practices Oversight and Management, reporting to Chief Operating Officer Scott Powell. In this role, he will establish an integrated and consistent approach to sales practice monitoring, analytics, and reporting across the company.

Cleary previously served as co-president of Santander Bank and head of Consumer and Business Banking at Santander US. He was on the CEO’s Executive Committee, the Sales Practices Committee, and the First and Second-Line Risk Committees and drove key regulatory initiatives. Among his accomplishments were developing the frameworks, policies and procedures, and governance to comply with regulatory guidance for safety and soundness, consumer protection, information security, regulatory compliance, and new business initiatives.

On Jan. 23, the Office of the Comptroller of the Currency announced a series of actions against former employees related to prior sales practices issues. In a companywide message, CEO and President Charlie Scharf said, “The OCC’s actions are consistent with my belief that we should hold ourselves and individuals accountable … At the time of the sales practices issues, the Company did not have in place the appropriate people, structure, processes, controls, or culture to prevent the inappropriate conduct … Over the past three years, the Company has made fundamental changes to its business model, compensation programs, leadership, and governance. We are committing all necessary resources to ensure that we operate with the strongest business practices and controls, maintain the highest level of integrity, and have in place the appropriate culture. The Company is different today, but we know we still have significant work to do to regain the trust of all stakeholders.”

On Dec. 2, we announced Scott Powell will become chief operating officer, a new position for the company, effective Dec. 9. As COO, Powell will oversee regulatory execution and relations, enterprise shared services, and a range of operational functions across the company.

Powell previously served as CEO of Santander Holdings USA and led its financial turnaround, including resolving significant regulatory issues, implementing customer-focused oversight programs, improving financial and operating controls and increasing community and employee engagement. Prior to Santander, Powell held a number of senior roles at JPMorgan Chase, including head of consumer banking, lending operations and consumer risk management. He also was CEO of consumer lending at Bank One, and he spent 14 years at Citi in various risk management roles.

Powell said, “I am truly excited about the opportunity to join Wells Fargo and take on this new role during a critical period in Wells Fargo’s history. Like Charlie, I have long admired and respected Wells Fargo. The company plays an important role in the U.S. economy, and we must ensure we are operating seamlessly and with the utmost integrity.”

On Nov. 20, Ray Fischer was named head of Cards, Retail and Merchant Services, effective Nov. 25. Fischer has worked in financial services for nearly 40 years, including 14 years at JPMorgan Chase as chief financial officer of Card, Merchant Services & Auto Finance. Following that, he was vice chairman and administrative officer of the Kessler Group and, most recently, was senior advisor to the Aries Financial Group.

On Nov. 7, we announced William M. Daley as Vice Chairman of Public Affairs, effective Nov. 13.

Dale’s career includes two cabinet-level appointments – Chief of Staff to President Barack Obama and Secretary of Commerce in the Clinton administration. In addition, he served as Vice Chairman of BNY Mellon and a member of the bank’s Executive Committee, as Vice Chairman and a member of the Executive Committee at JPMorgan Chase, and as President of SBC Communications (now AT&T).

“I am excited to be able to help with Wells Fargo’s continued transformation and to help shape the bank’s relationship with its customers, regulators and the U.S. public. I look forward to working with a talented executive team to make the new vision for the bank a reality,” said Daley.

On Oct. 17, we announced that Richard (Dick) Payne Jr. will join the company’s Board of Directors, effective immediately, and will serve on the Board’s Credit Committee. Payne retired in 2016 as vice chairman of Wholesale Banking at U.S. Bancorp.

On Sept. 27, the Board of Directors announced it named Charles W. Scharf as the company’s chief executive officer and president, and a member of the Board of Directors, effective October 21. Scharf was chairman and CEO of Bank of New York Mellon.

Scharf said, “I am honored and energized by the opportunity to assume leadership of this great institution, which is important to our financial system and in the midst of fundamental change. I have deep respect for all the work that has taken place to transform Wells Fargo, and I look forward to working closely with the board, members of the management team, and team members. I am committed to fully engaging with all of our stakeholders including regulators, customers, elected officials, investors, and communities.

On March 28, the Wells Fargo Board of Directors elected Allen Parker, previously General Counsel, as interim CEO and president upon Tim Sloan’s retirement. Parker joins the Board as it begins the external search for a permanent CEO and president.

On March 12, Wells Fargo CEO Tim Sloan appeared before the House Financial Services Committee to detail significant progress in the company’s transformation.

“The past few years have taught us that our company does well by doing right. But doing right does not stop with simply repairing harm and rebuilding trust,” Sloan said in his opening statement. “It is an ongoing commitment by all of Wells Fargo’s 260,000 team members — starting with me — to put our customers’ needs first; to act with honesty, integrity, and accountability; and to strive to be the best bank in America.”

On Jan. 30, we published a comprehensive Business Standards Report detailing the many changes Wells Fargo has made since 2016 to address root causes of past issues and transform the company.

We appreciate and value feedback we received on the report from the Interfaith Center on Corporate Responsibility, our Stakeholder Advisory Council, and other stakeholders.

On Jan. 27, the first print ad in a new integrated marketing campaign called “This is Wells Fargo” ran in national, local, and African American publications.

Over the past two years, we have undertaken a massive effort to transform Wells Fargo, and that includes keeping customers and stakeholders informed about ongoing progress.

This ad provides greater insight into the very real changes Wells Fargo has made and continues to make as a company — the ongoing operational and organizational transformation and the renewed focus on our customers, team members, and communities.

Wells Fargo CEO Tim Sloan sent a message to all team members in the Charlotte, North Carolina, area on Jan. 6, sharing his perspective on a Charlotte Observer editorial. He also responded directly to the newspaper on Jan. 7.

“Make no mistake, we know there is more work to do and historical matters to resolve, but our progress in the past two years is real and is continuing. Our team members are focused on this path forward and we are, together, building a better Wells Fargo.

I thank our customers and partners for their loyalty and support, our stakeholders for their engagement, and our team members for their passion and commitment to deliver on our vision. Despite the view of your editorial board, we come to work every day proud to serve this great city and help our customers succeed. Our pride and dedication will only continue to strengthen and grow across Wells Fargo, including right here in Charlotte.”

As part of settling matters and moving forward, on Oct. 22 we announced an agreement with the Office of the Attorney General of the State of New York to resolve claims alleging certain misstatements and omissions in disclosures related to sales practices matters.

“We are pleased to reach this agreement. Wells Fargo did not admit liability, and we believe that putting this matter behind us is in the best interest of all of our stakeholders, including customers. The settlement costs have been previously accrued.

We are making strong progress in our work to rebuild trust, and this represents another step forward. Over the past two years, we have made fundamental changes to retail sales practices, and the claims in this settlement relate to past product sales goals that were eliminated in 2016. We remain focused on transforming Wells Fargo into a better company for our customers and other stakeholders.”

On July 20, the Office of the Comptroller of the Currency announced that Wells Fargo has successfully completed the requirements of a consent order from September 2016 related to compliance with the Servicemembers Civil Relief Act.

“We are proud to serve those who serve our country. Satisfying the consent order reaffirms Wells Fargo’s ongoing commitment and continued work to reestablish itself and provide the service and advice our customers deserve.” –CEO Tim Sloan

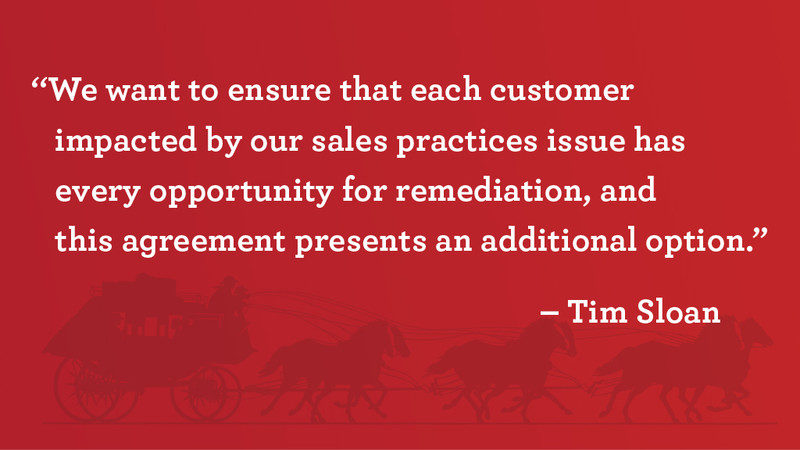

On June 14, the U.S. District Court for the Northern District of California approved a $142 million class-action lawsuit settlement known as Jabbari v. Wells Fargo Bank, N.A. The settlement class consists of all individuals who claim that Wells Fargo opened, without their consent, a consumer or small business checking or savings account or unsecured credit card or line of credit, or enrolled them, under certain circumstances, in Identity Theft Protection services, in each case between May 1, 2002, and April 20, 2017.

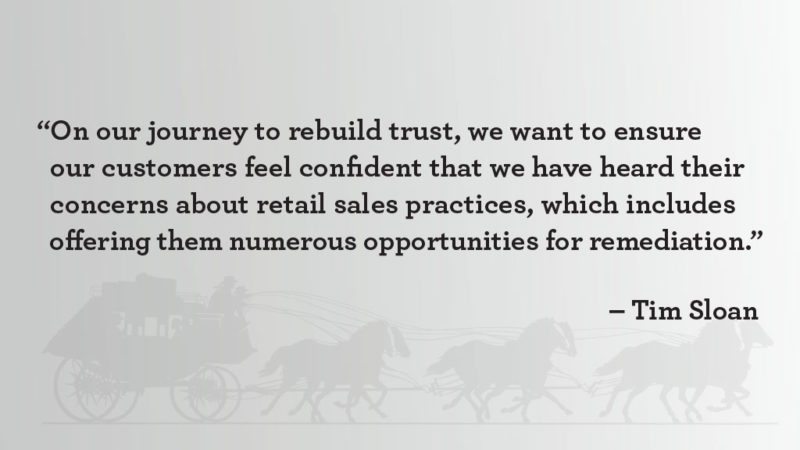

“We are pleased with this decision as it supports our efforts to help customers impacted by improper retail sales practices and ensures they have every opportunity for remediation,” said CEO Tim Sloan.

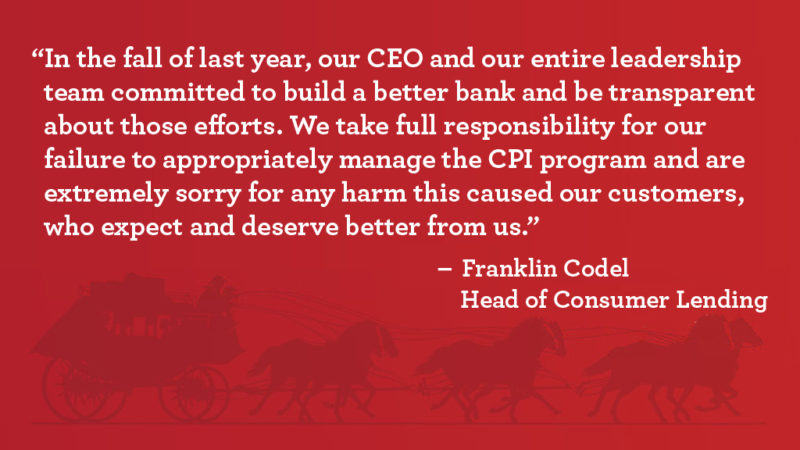

On April 20, we announced consent order agreements with the Office of the Comptroller of the Currency (OCC) and the Consumer Financial Protection Bureau (CFPB) to address previously disclosed matters regarding certain interest rate-lock extensions on home mortgages and collateral protection insurance (CPI) placed on certain auto loans.

“For more than a year and a half, we have made progress on strengthening operational processes, internal controls, compliance and oversight, and delivering on our promise to review all of our practices and make things right for our customers,” said CEO Tim Sloan. “While we have more work to do, these orders affirm that we share the same priorities with our regulators and that we are committed to working with them as we deliver our commitments with focus, accountability, and transparency. Our customers deserve only the best from Wells Fargo, and we are committed to delivering that.”

On March 1, we filed our annual Form 10-K with the Securities and Exchange Commission, providing information on new and existing reviews and efforts under way to find and fix problems and rebuild trust.

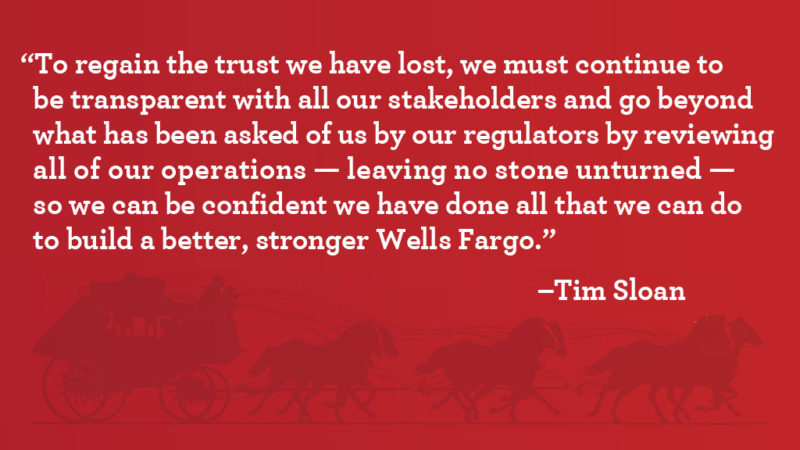

In a companywide message, CEO Tim Sloan said, “When we discover a problem, we are moving to find the root cause and fix it — so we can be confident we are doing all we can to build a better, stronger Wells Fargo.”

On March 1, we announced that John S. Chen, Lloyd H. Dean, and Enrique Hernandez, Jr., currently the board’s longest serving directors, and Federico F. Peña, who was scheduled to retire from the board in 2019, have decided to retire at the company’s 2018 Annual Meeting of Shareholders. As a result of these retirements, which are part of the board’s regular succession planning practices, the board will nominate 12 of its current directors for election at the company’s Annual Meeting of Shareholders, scheduled to be held on April 24, 2018.

On Feb. 2, we announced our commitment to satisfy the requirements of a new consent order we agreed to with the Federal Reserve. We will provide plans to the Federal Reserve within 60 days that detail what already has been done, and is planned, to further enhance our board’s governance oversight, and our compliance and operational risk management.

On Jan. 30, we announced that Sarah Dahlgren will join Wells Fargo as head of regulatory relations, effective March 12. Dahlgren will be responsible for oversight of regulatory relations for Wells Fargo’s Corporate Risk organization.

On Dec. 21, we announced the Stakeholder Advisory Council, which was formed to provide insight and feedback to the Board of Directors and senior management from the perspectives of our customers, team members, shareholders, and others.

On Nov. 29, we announced a newly formed Commitment to Customer Center of Excellence, which centralizes customer remediation efforts for consumer businesses effective Dec. 1. Headed by Joe Rice, the new group will cover the company’s Community Banking, Consumer Lending, and Payments, Virtual Solutions & Innovation businesses.

On Nov. 29, the Board of Directors announced it elected three new independent directors as part of its succession planning and refreshment process. With this announcement, the board has named six new directors in 2017 and a total of eight new independent directors since 2015.

On Oct. 12, we announced Mike Roemer will join Wells Fargo as chief compliance officer, effective January 2018.

On Oct. 3, CEO Tim Sloan updated the U.S. Senate Committee on Banking, Housing and Urban Affairs on changes he has initiated and overseen since becoming CEO last fall. Sloan once again apologized to customers and team members who were affected by improper sales practices and pledged to continue the transformative changes made across the company over the last year.

Read the written testimony >>

On Aug. 31, we announced the completion of an expanded third-party review of retail banking accounts dating back to the beginning of 2009. Combined with a class-action settlement (Jabbari v. Wells Fargo et. al.) and ongoing broad customer outreach and complaint resolution, the completed analysis further paves the way for making things right for customers who may have been harmed by unacceptable retail sales practices.

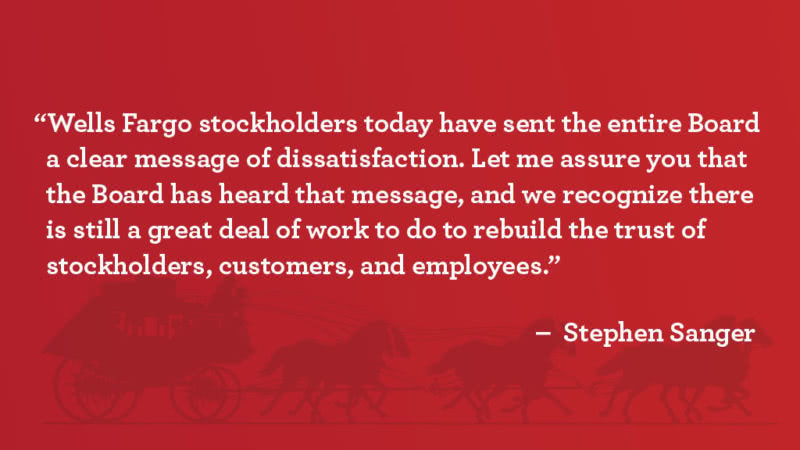

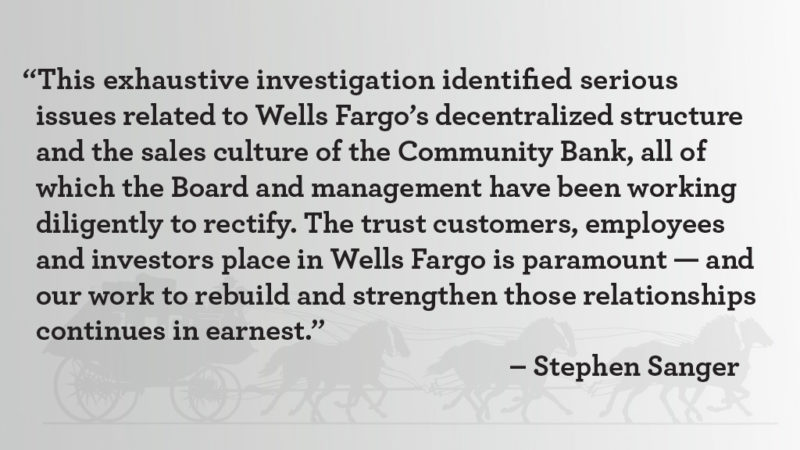

On Aug. 15, we announced several changes to our Board of Directors, including naming Elizabeth A. “Betsy” Duke to succeed Stephen W. Sanger as independent Chair, effective Jan. 1, 2018.

Additional actions include the retirement of three long-serving directors (including Sanger) at year-end 2017, and adding a new independent director and changing the composition of Board committees, both effective Sept. 1, 2017.

The Board also expects to elect up to three additional independent directors before the 2018 annual meeting while maintaining an appropriate balance of experience and perspectives on the board.

CEO Tim Sloan shared updates on the company’s efforts to rebuild trust and provided additional context on its latest quarterly SEC financial filing in a companywide message on Aug. 4.

On July 27, we announced steps we are taking to make things right for auto loan customers who may have been financially harmed due to issues related to auto Collateral Protection Insurance (CPI) policies.

In July 2016 we initiated a review of the CPI program in response to customer concerns and determined that certain external vendor processes and internal controls were inadequate. More important, we discovered that those deficiencies inadvertently harmed some of our customers. We discontinued the program in September 2016 and immediately started work, with the help of independent consultants, to ensure that our remediation plan addresses customer situations in a thoughtful way.

On July 8, the U.S. District Court of Northern California issued a court order granting preliminary approval of the class-action agreement for the improper retail sales practices lawsuit that was announced in March and expanded in April. (Jabbari v. Wells Fargo, N.A., et al.).

On June 8, we announced the consolidation of the Community Banking Regional President (RP) and Area President (AP) roles into a single position to help reduce levels of management and tighten controls in the Community Bank.

The news followed a robust May 24 announcement of new leaders and other organizational changes in the Community Bank—all part of the ongoing effort to put customers first, provide expert training to team members, and strengthen oversight of risk.

On April 25, Wells Fargo held its annual meeting of stockholders in Ponte Vedra Beach, Florida.

On April 21, we expanded our class-action settlement for retail sales practices, adding $32 million to the previous agreement and including any customer impacted since May 2002. This brings the total settlement amount to $142 million.

Read the news release>>

In a companywide video message on April 10, CEO Tim Sloan acknowledged the Board of Directors’ report as “thorough, candid, and tough,” and said it “offers lessons that will influence how we continue to build a better Wells Fargo for all of our stakeholders, including you, our team members.” Read the news release >>

On April 10, our Board of Directors released findings of its independent investigation of retail banking sales practices and related matters, which included additional compensation actions. Total compensation actions now exceed $180 million after the Board mandated additional forfeitures and clawbacks from the former CEO and former head of the Community Bank. Read the news release >>

On March 28, we announced an agreement in principle to settle a class action lawsuit that will compensate customers who claim that Wells Fargo opened an account in their name without their consent, enrolled them in a product or service without their consent, or submitted an application for a product or service in their name without their consent.

On March 7, we created three new teams and streamlined the structure of our retail bank to help drive efforts to rebuild trust and emphasize customer experience in our branches.

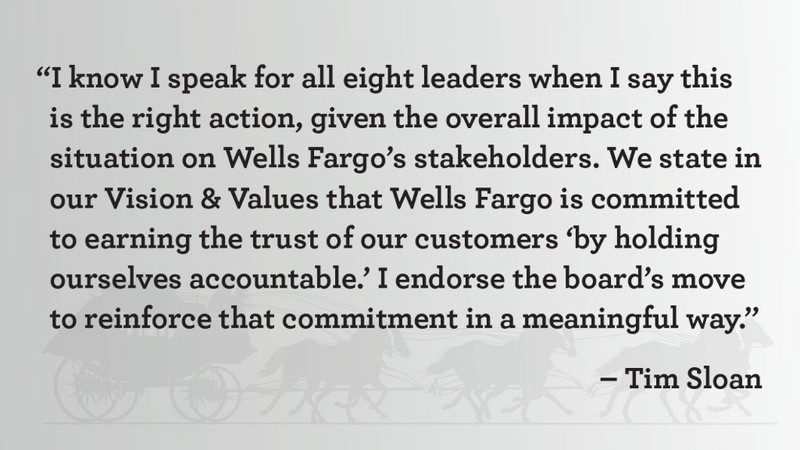

To reinforce the accountability of senior management for the overall operational and reputational risk of Wells Fargo, the Board — after discussion with CEO Tim Sloan — eliminated 2016 bonuses. It also reduced the payout of 2014 performance shares that vested following 2016 by up to 50 percent for the eight senior leaders who were on the company’s Operating Committee prior to November 1, 2016.

As part of its continuing review of committee responsibilities and oversight of risks, our Board made changes to enhance the risk oversight responsibilities of various Board committees, including the Risk Committee.

On Feb. 21, we announced the termination for cause of four current or former senior managers in our Community Bank, based on the Board of Directors’ ongoing independent investigation. As a result, those senior managers forfeited their 2016 bonuses and outstanding equity awards. None of these senior managers will be paid any severance.

On Feb. 20, our Board announced the election of two new independent directors — Karen Peetz and Ron Sargent — who bring financial services, client services, regulatory, and customer retail and marketing experience, as well as experience in the management of a large workforce serving customers globally through a variety of channels.

We created the Office of Ethics, Oversight and Integrity to centralize the handling of our global ethics and integrity program, internal investigations, complaints oversight, and sales practices oversight.

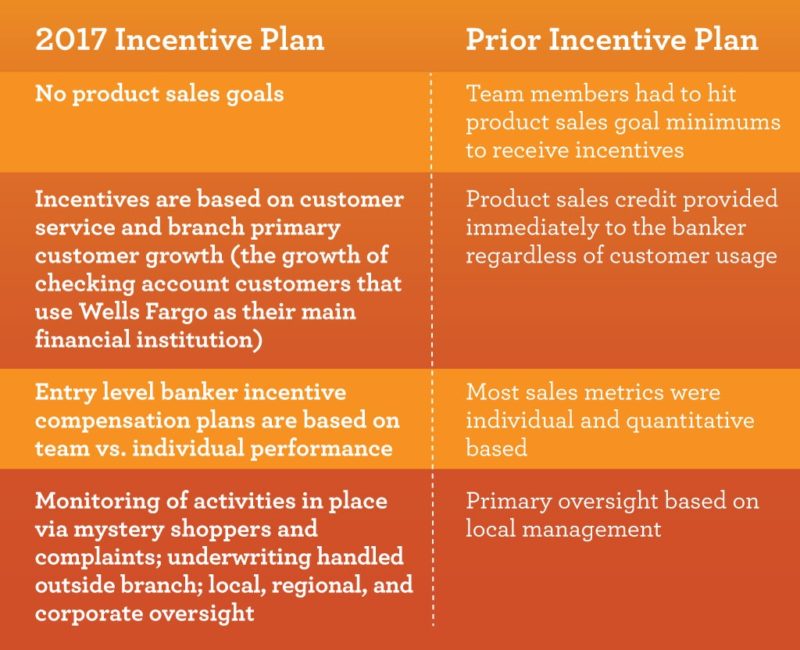

Effective Jan. 1, we put in place a new incentive compensation program for retail branch team members, including managers, tellers, and personal bankers.

By the end of 2016, we had reached out to approximately 40 million retail and 3 million small business customers through statement messaging, other mailings, and online communications, asking them to contact us with any concerns. We also refunded a total of $3.26 million to customers with accounts that we could not rule out as unauthorized. This includes the $2.6 million in refunds that were disclosed as part of the legal and regulatory settlements announced on Sept. 8, 2016.

Following engagement with our investors, the Board of Directors amended Wells Fargo’s by-laws on Nov. 29 to require that the chairman and any vice chairman of the Board be independent directors.

We launched a thorough review of and are making enhancements to our EthicsLine processes, with the support of a third-party expert.

We also expanded our “Raise Your Hand” initiative, encouraging team members to speak up when they see something unethical — or if they have an idea to help reduce risk.

On Nov. 10, CEO Tim Sloan announced “rebuilding trust” as a company priority in order to sharpen our focus on the task ahead, what our company and team members must accomplish together, and how best to serve our customers.

We began providing monthly updates on the impact of the sales practices matter on customer activity in our retail bank.

On Oct. 25, Tim Sloan hosted his first town hall as CEO and pledged to take the decisive actions required to rebuild trust.

Approximately 4,100 risk professionals who previously reported within various businesses were realigned to report into our central Corporate Risk Group to provide greater role clarity, increased coordination, and stronger oversight. An additional 1,100 risk professionals also will be realigned to report into Corporate Risk during 2017.

The move builds on ongoing efforts since 2015 to centralize human resources and other departments to improve oversight, accountability, and controls.

Senior leaders began a robust “Conversations Tour” internally to address concerns of team members in communities across the U.S. and to collect their thoughts on how to build a better Wells Fargo for the future.

The Board of Directors separated the roles of chairman and CEO on Oct. 12, and elected Steve Sanger as independent chairman and Elizabeth Duke as independent vice chair.

On Oct. 12, John Stumpf retired as chairman and CEO.

The Board elected Tim Sloan as CEO and a director. He retained the title of president.

On Oct. 10, we announced multiple changes to Wells Fargo’s Operating Committee — the company’s highest-ranking executives — including a new leader for Consumer Lending, a new leader for Wholesale Banking, and the formation of a new Payments, Virtual Solutions and Innovation Group.

The changes built on a July 12 announcement naming Mary Mack as the new head of Community Banking.

On Oct. 1, we eliminated product sales goals for retail bank team members who serve customers in our bank branches and call centers.

In testimony with the U.S. House Financial Services Committee on Sept. 29, former CEO John Stumpf shared an update on our actions to address wrongful sales practices and announced we would accelerate the elimination of product sales goals in our retail bank from Jan. 1, 2017 to Oct. 1, 2016.

Pursuant to our sales practices settlements, we developed a program to offer mediation services at no charge to customers who believe we have not adequately resolved their complaints involving potentially unauthorized accounts.

Mary Mack, head of Community Banking, created a new Change Leader position to redefine the business model in branches and call centers to focus on the customer experience.

On Sept. 27, our Board announced that former CEO John Stumpf and the Board agreed that he would forfeit all of his unvested equity awards (valued at approximately $41 million) and would forgo his salary while the Board’s investigation is pending.

The announcement also communicated that Carrie Tolstedt, former head of the Community Bank, had left the company; the Board determined that she would forfeit all of her unvested equity awards (valued at approximately $19 million). Tolstedt agreed not to exercise any of her fully vested stock options while the Board’s investigation is pending.

In addition, the Board determined that Stumpf and Tolstedt would not receive 2016 bonuses.

On Sept. 27, the Independent Directors of the Board launched a comprehensive, independent investigation into Wells Fargo’s retail banking sales practices and related matters.

On Sept. 20, in a hearing with the U.S. Senate Banking Committee, we announced we would voluntarily expand our reviews of retail and small business accounts to include 2009 and 2010, in addition to account reviews for 2011 to 2016 required under our consent orders. These reviews, as well as our ongoing data analysis, could lead to, among other things, an increase in the identified number of potentially impacted customer accounts.

On Sept. 13, we announced we would eliminate product sales goals in our retail bank beginning Jan. 1, 2017.

We created an online resource page and a dedicated hotline to answer questions and address concerns for customers.

We announced regulatory and legal settlements related to improper sales practices in our retail bank.